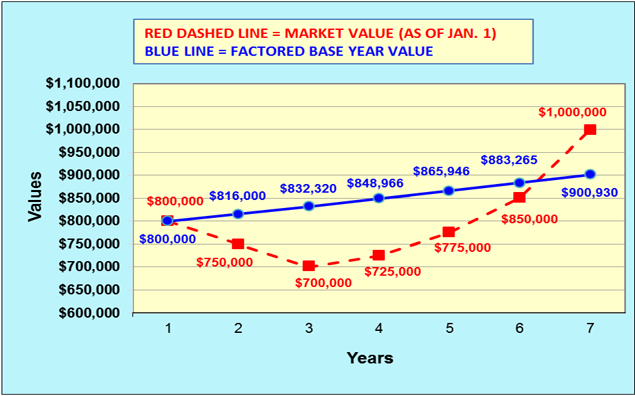

The example below shows when a property owner would qualify for a temporary reduction.

In the example a property owner purchases a property at fair market value for $800,000 establishing the base year value at year 1. On the subsequent lien date (year 2), the market value decreases to $750,000, but the property owner‘s assessment is based on the factored base year value, $816,000 ($800,000 plus 2%) which is higher than the market value. Therefore, the property owner would qualify, under Prop 8, for a temporary reduction to $750,000.

In this case, the property owner would qualify for a Proposition 8 reduction, for years 2 through 6, but not in year 7.

Note: In year 7, the factored base year value, $900,930, would be reinstated and the property owner would not qualify for relief under Prop 8

The red line: the “market value,” the current market value based on sales of comparable properties as of January 1 of that year.

The blue line: the “factored base year value,” purchase price plus no more that 2% factoring per year.